Our customers have told us what is important to them, and we have made it our business to keep looking for new ways to expand on our offering and services.

June 2024 – Market Update

Market Update – June 2024

Low wind and gas production had an impact on prices across the National Electricity Market in June, while New South Wales normalised after a challenging May.

Spot Market

In the spot market, prices were impacted by low wind production in the southern states, as well as increased gas prices due to low gas production and system-wide constraints.

At the same time, colder weather drove up demand across the board, leading to higher prices in Queensland (finishing up $31.98 at $124.67) and Victoria (up $31.26 at $164.23).

Despite these factors, prices in New South Wales actually fell – closing the month down $120.81 at $152.75. This reflects the state’s extremely high spot prices in May, which were partly driven by line constraints and outages that were resolved by June.

Contract market

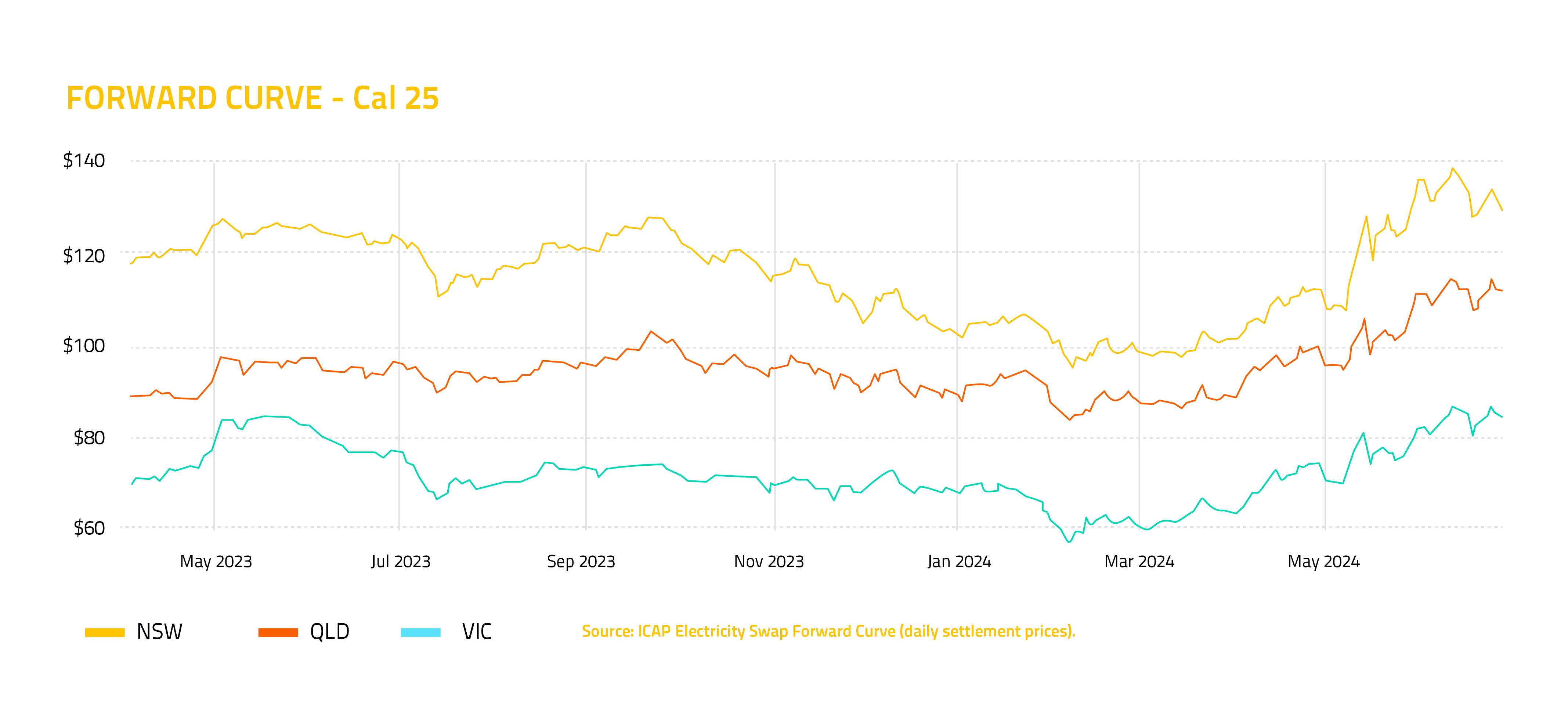

Prices in New South Wales also fell in the contract market, with the Cal 25 price finishing the month down $6 at $130.40. Again, this says more about the volatility New South Wales experienced in May than it does about conditions in June.

In Queensland and Victoria, the ongoing wind droughts and high gas prices that pushed up spot prices in those states also drove Cal 25 prices higher – up 55 cents in Queensland (at $112.10) and up $3.10 in Victoria (at $84.35).

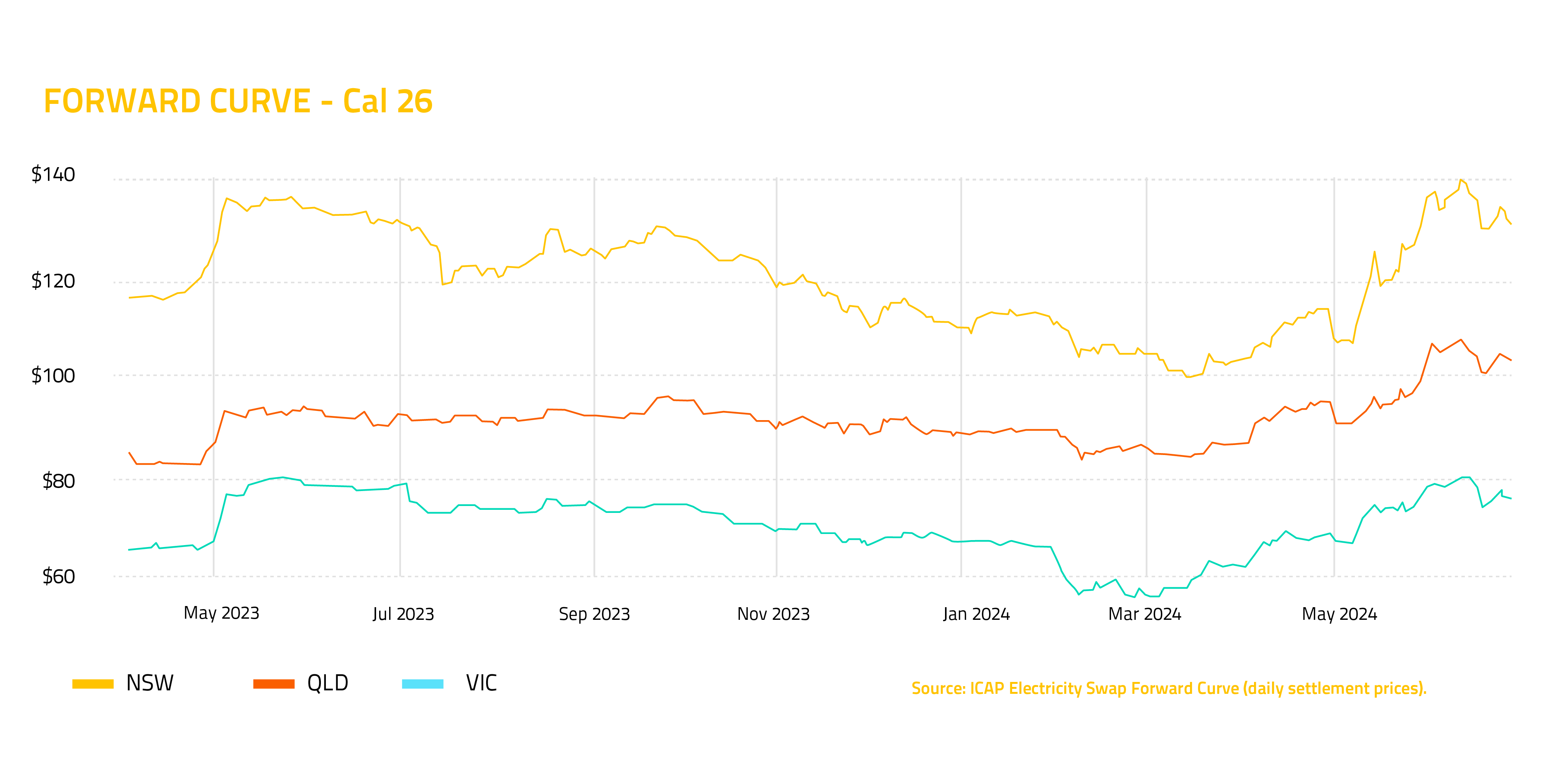

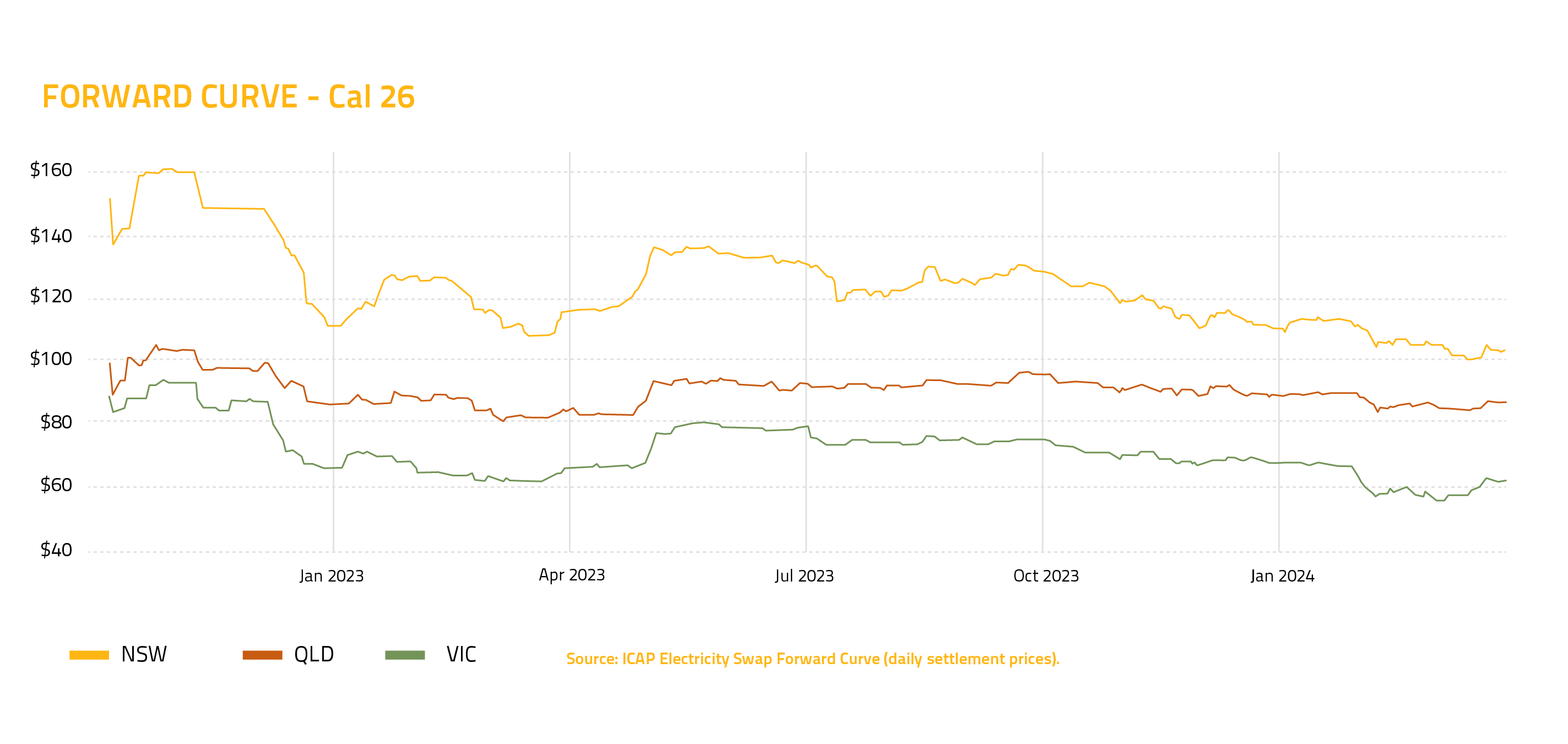

The drop in New South Wales prices rippled through to Cal 26, down $5 at $131. There was little volatility otherwise, though, with the Queensland Cal 26 price finishing the month up 5 cents (at $103.40) and Victoria finishing down $1.95 (at $76).

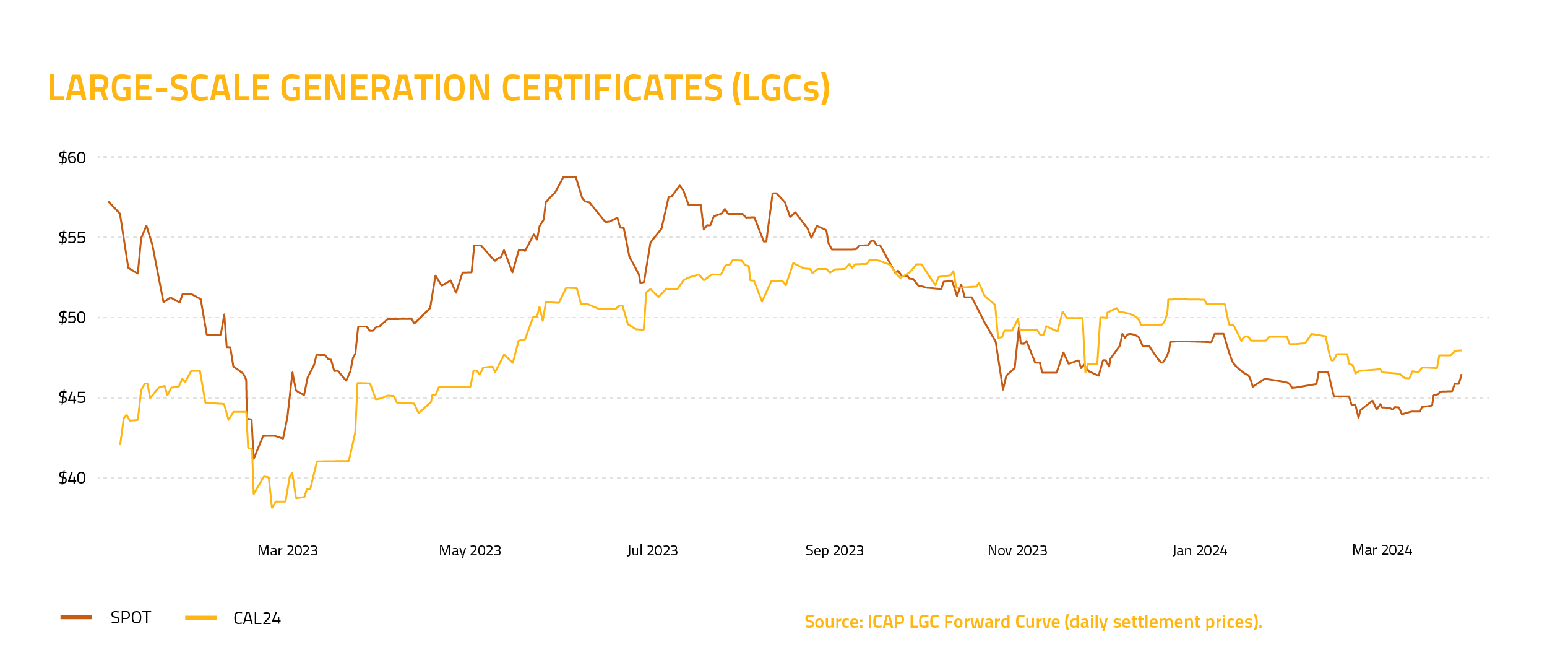

Environmental market In the environmental sector, we saw high levels of liquidity in the market for Large-Scale Generation Certificates (LGCs). This placed downward pressure on prices, which finished the month down 50 cents at $45.50.

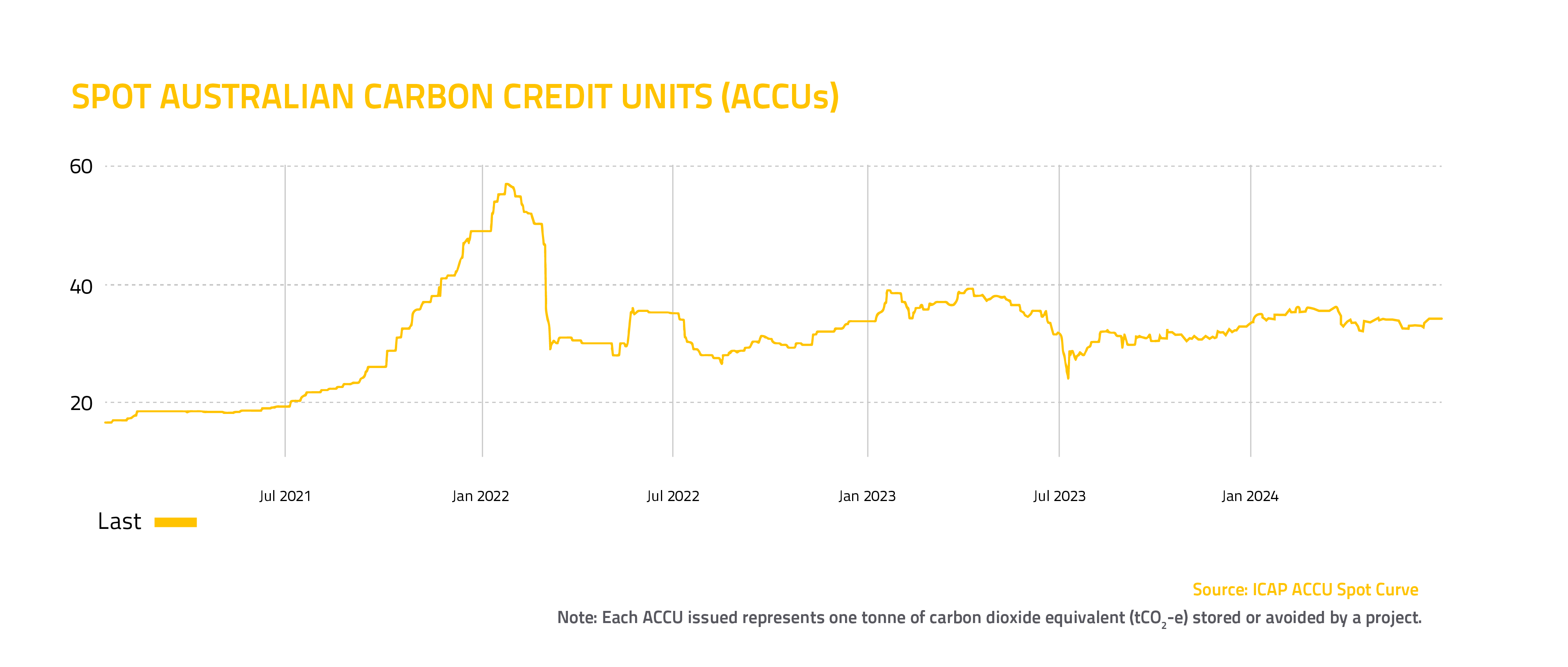

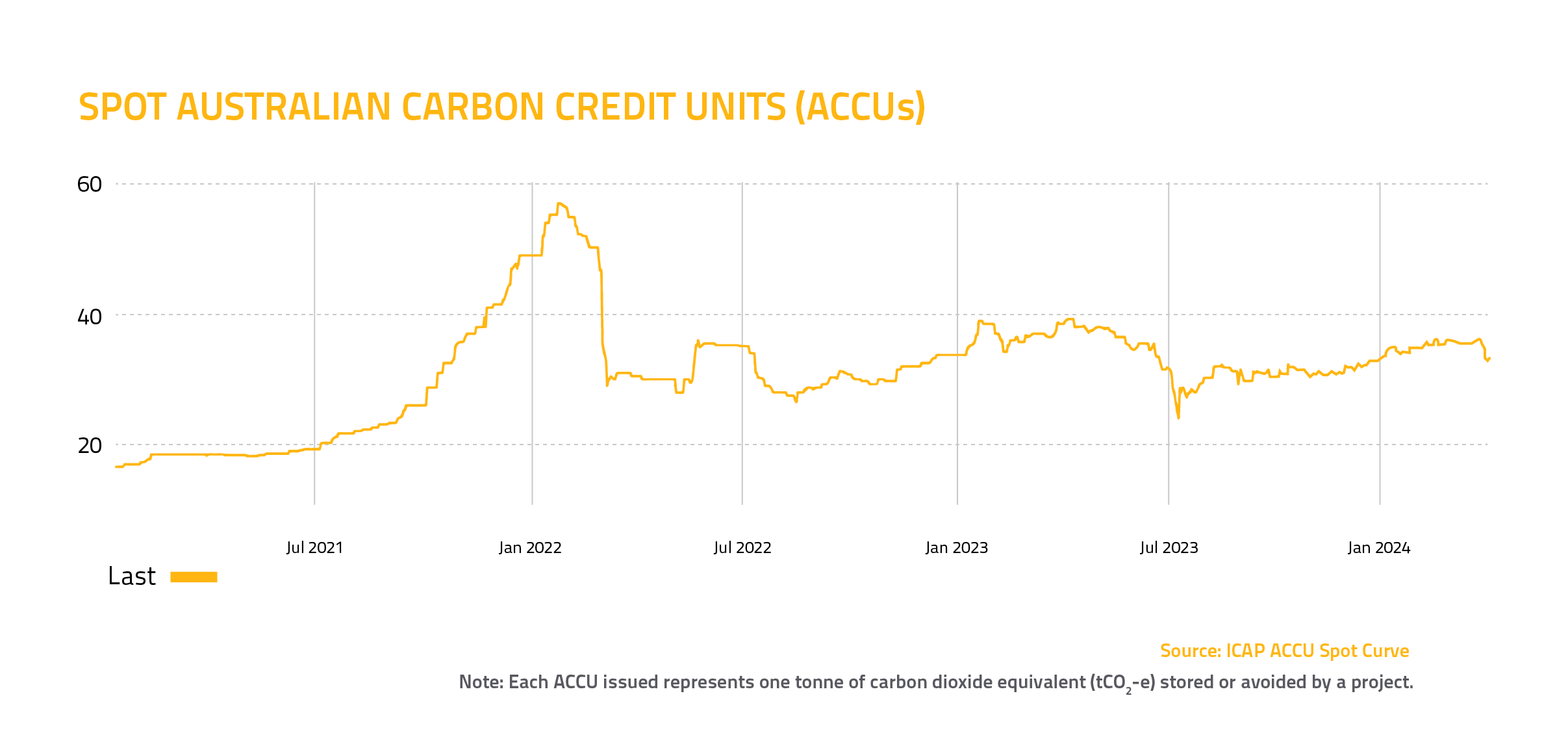

Meanwhile, renewed buying interest in the carbon market drove up the price of Australian Carbon Credit Units (ACCUs), which closed $1.25 higher at $34.25.

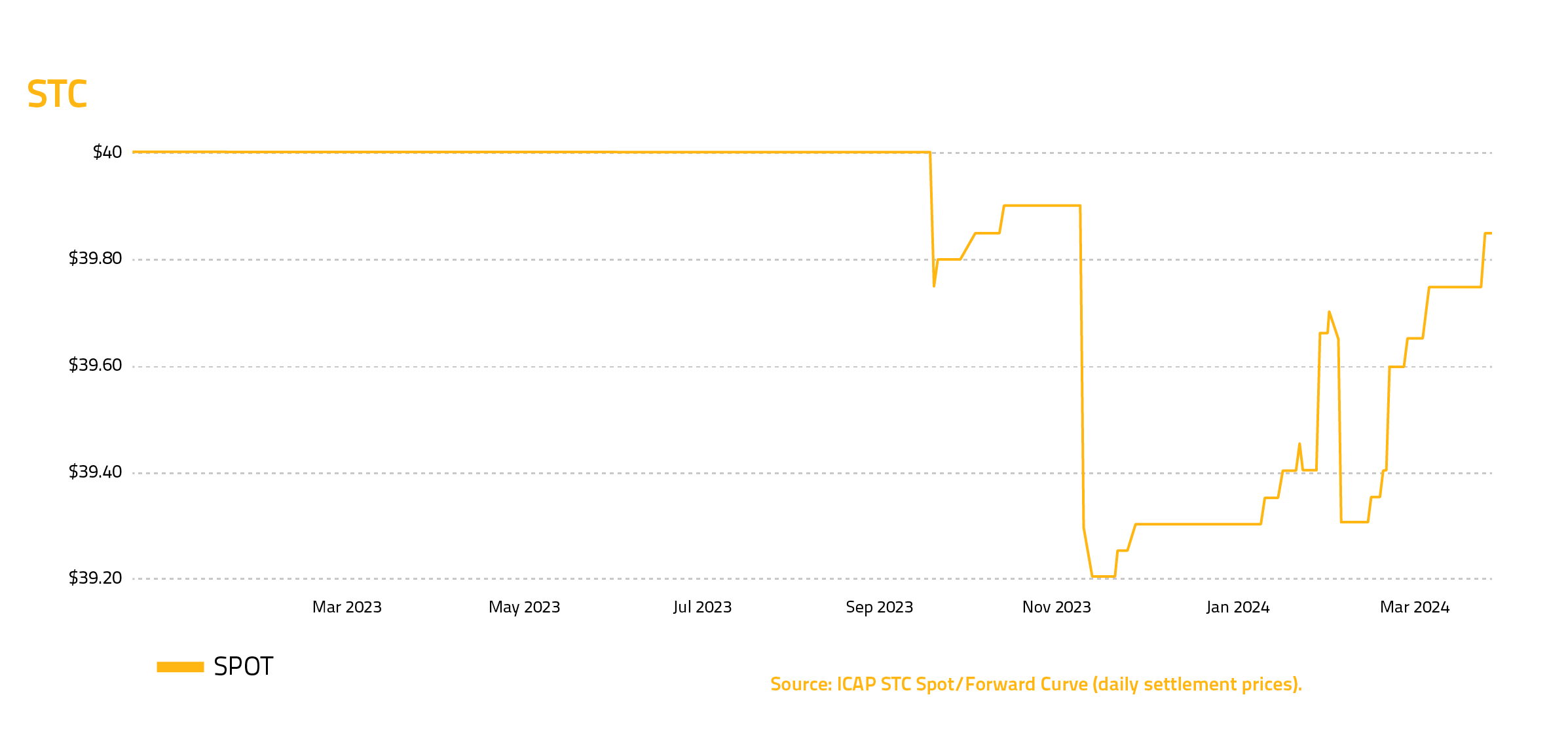

The Clearing House for Small-Scale Technology Certificates (STCs) returned to surplus, but trading stayed close to the Clearing House price of $40 at $39.90.

By the end of the month, the Clearing House was only in surplus by about 6,000 certificates, indicating a likely return to deficit by the Q2 surrender deadline on July 28.

And that’s another recap of the month.

If you’d like to learn more about how we can add value to your business or support your decarbonisation goals, please reach out to our team.

Have a great month ahead, and we’ll see you here again next month.

April 2024 – Market Update

Market Update – April 2024

Spot prices were on the rise in the energy market this month – and that had a flow-on effect for the forward market.

Spot market

In the spot market, unit outages and low winds lead to rising prices across the National Electricity Market. The spot price finished up $10.66 in Queensland (at $84.75), up $19.42 in New South Wales (at $89.89), and up $32.76 in Victoria (at $84.75), where wind makes up a larger proportion of generation.

Contract market

Those higher-than-expected prices in the spot market have also had an impact on the contract market.

Bullish sentiment saw the curve push up considerably throughout the month, but it cooled off somewhat on the last day of April, following reports that Australia’s largest coal-fired power station will remain open past its expected closure date in 2025. Cal 25 prices ultimately finished up $8.75 in Queensland (at $97.50), up $8.20 in New South Wales (at $109.55), and up $8 in Victoria (at $72.20).

When we look ahead to Cal 26, we can see that same sentiment leading to similar price increases across the board, finishing the month up $5.70 in Queensland (at $93.25), up $6.65 in New South Wales (at $110.15), and up $6 in Victoria (at $68.75).

Environmental market

In the environmental market, an increase in buying demand has put upward pressure on prices for both Large-Scale Generation Certificates (LGCs), finishing up 10 cents at $46.35.

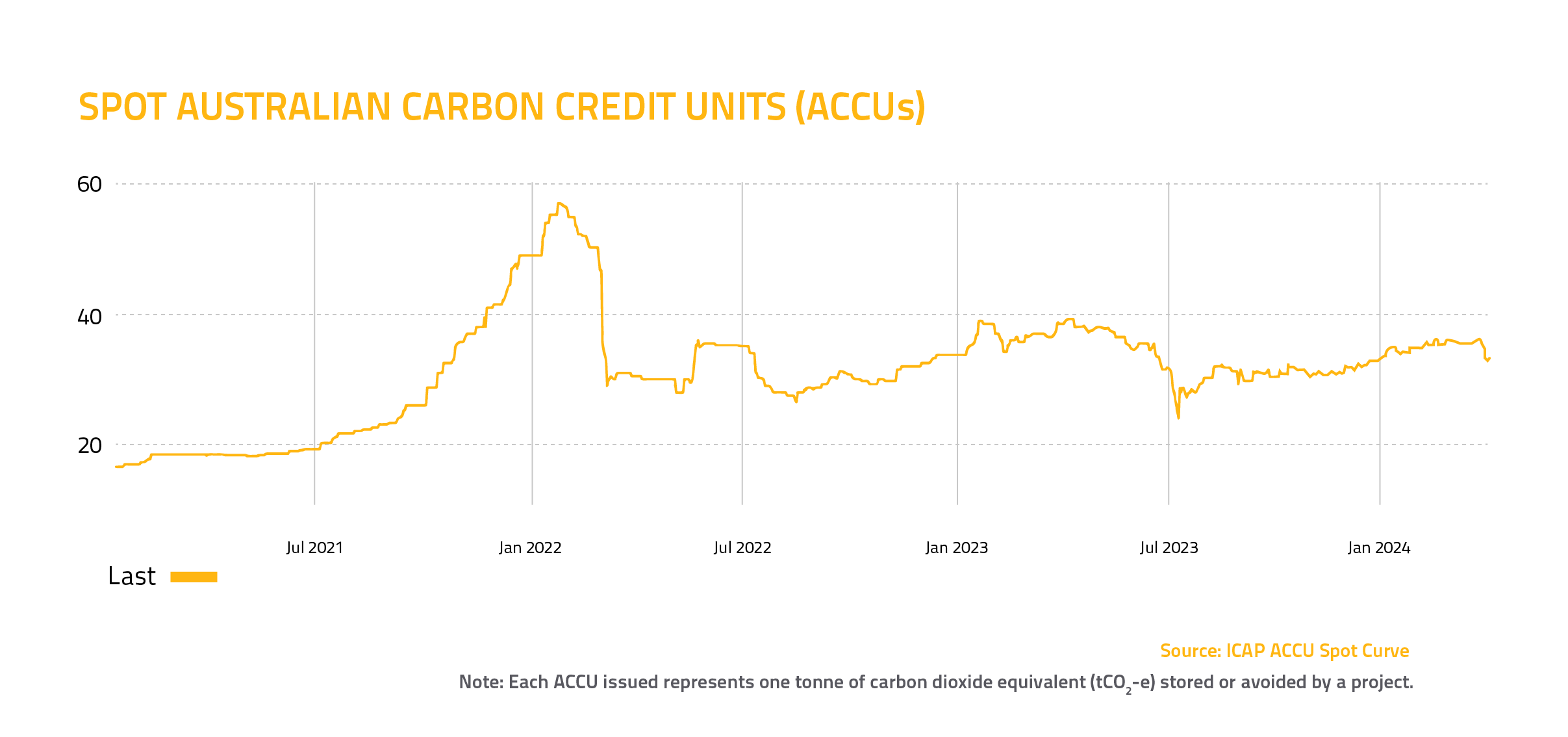

Australian Carbon Credit Units (ACCUs) also closed higher, up 75 cents at $34.

The clearing house for Small-Scale Technology Certificates (STCs) returned to deficit close to the Q1 surrender deadline. That led STC creators to sell to the clearing house, rather than engage in wholesale trading, resulting in a price increase – finishing up five cents at $39.90.

And that’s it for April! We look forward to seeing you for another market update next month.

March 2024 – Market Update

March was a relatively uneventful month in the energy market, but a busy month for the Stanwell Energy team, as we took to the road with our new Progressive Purchasing Portal.

Throughout the month, our Retail team visited our partners and consultants in Brisbane, Sydney and Melbourne to demonstrate our brand new Progressive Purchasing Portal.

The Portal allows our customers to submit offers to purchase energy online at live market prices, at their own convenience, progressively throughout the life of their contract.

Our portal puts the power back in your hands, by allowing you to purchase energy when you choose. This will only enhance the experience for our valued customers, making the purchasing process more accessible, convenient and manageable.

If you missed out on one of these presentations, please reach out to us for a demonstration!

Now, let’s take a look at the state of the market in March.

Spot market

In the spot market, we saw prices fall across the board – closing at $74.09 in Queensland (down $45.64), $70.47 in New South Wales (down $41.20), and $51.99 in Victoria (down $30.95).

This was mainly due to high unit availability in Queensland, New South Wales and Victoria. At the same time, we had relatively mild weather in all three states. That helped to drive down demand, and prices fell accordingly.

Contract market

In the contract market, low liquidity and less volume trading overall in generic baseload swaps had led the curve to drift downwards in February.

That drop in price led to a bit of buying in March – enough for prices to go up slightly, finishing the month at $88.75 in Queensland (up 50 cents), $101.35 in New South Wales (up $2.35), and $64.20 in Victoria (up $3.40) – but not enough to really move the needle this month.

Looking ahead to Cal 26, prices are similarly flat. In Queensland, the Cal 26 price finished the month at $87.55, up $1.60.

In New South Wales, continued speculation on the lifespan of Australia’s largest coal-fired power station led to a slight drop in price – closing at $103.50, down $1.55.

In Victoria, where Cal 26 prices have been on the decline for months, we saw the back end crawl up to be more in line with the Cal 25 price – closing at $62.75, up $5.75.

This follows an incident in February that saw extreme winds topple six of the state’s high voltage transmission towers. That led to a sharp, sudden rise in the spot price, which seems to have spurred some interest in the forward market there.

Environmental market

In the environmental market, an increase in retail buying led to a small uptick in prices for Large-Scale Generation Certificates (LGCs), which closed the month at $46.25 (up 50 cents).

Small-Scale Technology Certificates (STCs) saw a similarly slight price increase, closing at $39.85 (up 20 cents).

Speculation around the supply of Australian Carbon Credit Units (ACCUs) led the price of those units to rally throughout the month. But as those rumours cooled off, so did ACCU prices, ultimately closing at $33.25 (down $1.75).

And that’s it for March! We look forward to seeing you for another market update next month – and don’t forget to get in touch if you want a demonstration of our Progressive Purchasing Portal in the meantime!